Smart buildings should target worker productivity

- June 19, 2020

- imc

Smart building technology can make the biggest savings by targeting human productivity, according to Rethink Technology Research.

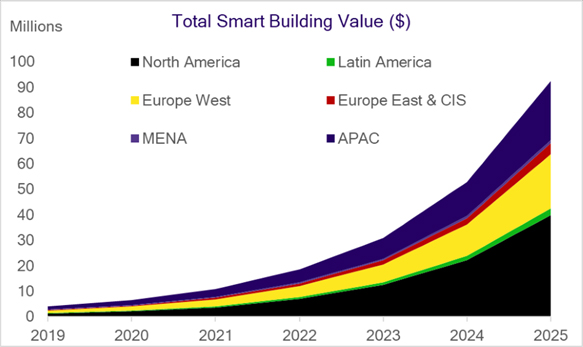

The global smart building market is set to hit $92.5bn by 2025, driven by worker productivity goals, says the report. It found that smart building penetration of the total commercial and industrial building stock will only reach 0.49% in the period, with huge room to grow.

The smart building market globally was around $4.2bn in 2019, with the primary driver being the desire to improve the productivity of the workers that are housed within those buildings’ walls. In most instances, the costs of occupying a building in terms of square metres, human capital is almost always the largest single component.

To this end, to use smart building technologies to save costs or increase margins, the main use case targeted should be human productivity, says the report. While the technologies can help manage operating costs, such as energy bills, or provide improved services such as secure access or usage analytics, on a per-dollar basis, these should not be the priority targets for new installations.

This, says the report, is something of a surprise for many in the technology markets.

“We are accustomed to IoT technologies being used for process or resource optimisation, such as smart metering providing better purchasing information for energy providers, or predictive maintenance helping to reduce operational costs and unplanned downtime,” said a Rethink statement. “This line of thinking is not typically extended to human workers however but, when you evaluate how buildings are used, it becomes clear that getting more out of your workforce is a better use of your budget. To this end, the IoT technologies needed to better understand and optimise a building’s internal processes and the patterns of its workers are vital, and will account for a large number of the devices installed in the smart building sector.”

The report refers to the 3-30-300 Rule, which was popularised by real estate firm JLL. The gist is that for every square-foot (0.09 square metres) of space that a company occupies in a building, it will spend $3 annually on utilities, $30 on rent and $300 on its payroll. This ratio shows how smart building efforts should be coordinated. A 100% efficiency improvement would only save $1.50 per square-foot per year, which is the equivalent of a 0.5% change in the payroll costs.

Using the rule, JLL argued that to reduce employee absenteeism by 10%, this would equate to $1.50 per square-foot annually, and a 10% improvement in employee retention would translate to an $11 per square-foot annual saving. To increase employee productivity by 10%, this would translate to $65 per square-foot per year, and it points to the World Green Building Council’s (WGBC) decree that an 18 to 20% improvement is quite easily achieved in the right environment.

The WGBC published a quite influential meta-study in 2013 that combined the findings of dozens of other pieces of research to examine the impact of sustainable building design on employee health. JLL was interested in this from the productivity perspective, and the WGBC found that eight primary factors had direct positive impacts on building occupants – in this case, workers.

The factors include natural light, good air and ventilation, temperature controls, views, and green spaces. The WGBC then posited that the following increases in productivity could be achieved by making better use of the factors: better lighting (23% increase), access to green natural spaces (18%), improved ventilation (11%), and individual temperature control (3%). JLL calculated the returns based on an algorithm some of its real estate brokers developed, but those figures aren’t applicable to every building or task.

Payroll, in the commercial sector at least, is usually more than 80% of a company’s operating costs, often closer to 90%. Industrial output has more materials costs, and so JLL’s rule is not so applicable. However, given the commercial sector accounts for around 63% of global GDP, with industry on 30% and agriculture at about 7%, the rule is quite useful for evaluating the value of smart buildings across the spectrum.

“To this end, if a company has a given budget to invest, it seems prudent to spend that cash on trying to make employees more productive, rather than save on energy bills,” said the statement. “That’s a message that isn’t going to go down well in this environmentally-charged climate but, thankfully, many of the energy providers and associated systems integrators will install demand response (DR) and automation technologies through regular upgrade and replacement cycles, which will help optimise energy usage in these buildings.”

Collectively, buildings and construction account for around 30 to 40% of global energy use and energy-related carbon dioxide emissions. Because of this, the per square-foot energy efficiency of buildings needs to improve by around 30% to meet the Paris Agreement environmental targets. By 2060, it is expected that the total buildings sector’s footprint will have doubled, reaching around 230bn square metres.

This forecast examines the value of smart building technology globally, covering the proportion of the hardware that can be directly attributed to smart buildings, the associated software and management platform services, and installation and management related consulting. It does not try to forecast the total value created by the technology, nor the installation and upkeep revenues. That would be such a large number that it would not be useful.

In terms of market variation, Rethink expects North America and Western Europe to be the strongest initial market, with parts of Apac (China, Japan and South Korea) making up for the rest of that region’s low adoption. This is a pretty similar story to many of its other IoT forecasts, and there is not really reason to think this one will be markedly different.

“This is a trend that is going to take longer to emerge too, and we expect the years immediately after the forecast period to post some impressive growth,” said the statement. “We foresee this market being more gradual than the explosive growth curves seen in other IoT markets, but due to its potential size, this slower penetration is not to be seen in a negative light.”

This report is for those at C-suite and strategy level that are trying to improve profit margins in buildings, whether that is in the managerial and human resources realm or in the operations and facilities management side. This report is aimed at anyone running industrial or commercial buildings, those who employ large workforces, and any equipment and service providers that would sell into those markets.

Companies mentioned in this report are ABB, Advanced Control Solutions, Airedale, AWS, Bajaj Electricals, Bosch, Boss Controls, Building Logix, Centrica, Cisco, Cylon, Delta Controls, Engie, Enel, Entelec, Eon, Google, GridDuck, Hitachi, Honeywell, HPE, IBM, Intel, Johnson Controls, Legrand, Microsoft, NEC, Oracle, Osram, Panasonic, PTC, Sage, Salesforce, SAP, Schneider Electric, Siemens, Signify (Philips), Spaceti, Trend, United Technologies and Verdigris.